Step-by-Step Home Loan Process in India (2026): Documents, Approval & Timeline

Buying a home is one of the biggest financial decisions for most Indians. But while lenders advertise low interest rates and quick approvals, very few explain what actually happens after you apply. How do banks decide your housing loan eligibility? Why do some applications get delayed during property verification? If you are applying for a home loan or planning to, you must learn the home loan process step by step.

Let us understand in detail!

What is a Home Loan and How Does It Work?

A home loan is a secured loan offered by banks and housing finance companies to help individuals buy, construct, renovate, or expand a residential property. The lender provides a loan amount based on your income, repayment capacity, credit score, and property value.

In India, home loans are regulated by:

- RBI (for banks)

- NHB (for HFCs, now merged with RBI in 2019)

In a home loan, the property acts as collateral until the loan is fully repaid. Borrowers repay the loan through monthly EMIs over a fixed tenure that may extend up to 30 years.

Understand the different types of loans so you can choose the one that fits your next financial move.

What Are the Steps in the Home Loan Process?

When you apply for a home loan, lenders assess your income, repayment capacity, credit history, property documents, and legal clearances before approving the loan.

| Step | Process |

| 1 | Check housing loan eligibility |

| 2 | Submit the home loan application |

| 3 | Share income, KYC, and property documents |

| 4 | Complete credit and document verification |

| 5 | Property legal and technical checks |

| 6 | Receive the home loan sanction letter |

| 7 | Sign the loan agreement |

| 8 | Complete the home loan disbursement process |

| 9 | EMI repayment begins |

Here is the detailed step-by-step guide:

Step 1: Check Housing Loan Eligibility

Before applying, most lenders assess an applicant’s housing loan eligibility based on:

- Income and repayment capacity

- Age

- Employment type (salaried, self-employed, or business owner)

- Existing liability

- Credit history (CIBIL score)

For example, salaried individuals in metro cities are typically eligible for loans of up to 60 times their monthly income, depending on deductions and existing EMIs. For self-employed professionals, lenders examine net profits from audited financials.

Step 2: Application Submission

Once eligibility is checked, the borrower submits the home loan application online or offline. The application includes personal details, employment information, income details, preferred loan amount, tenure, and property information.

At this stage, the lender charges a processing fee, usually 0.25% to 1% of the loan amount, either upfront or post-sanction.

Step 3: Share Required Home Loan Documents

Borrowers must submit KYC, income, bank, and property-related documents for verification.

Commonly required documents include:

| Document Type | Examples |

| Identity Proof | PAN card, Aadhaar card, passport, voter ID |

| Address Proof | Aadhaar, utility bill, rental agreement, passport |

| Income Proof | Salary slips, Form 16, ITRs, profit & loss statements |

| Bank Statements | Last 6–12 months bank statements |

| Employment Proof | Employee ID, offer letter, business registration proof |

| Property Documents | Sale agreement, title documents, approved building plan, builder NOC |

Note: Incomplete or incorrect documents can delay the home loan process.

Step 4: Complete Credit Verification

After document submission, the lender verifies the applicant’s financial profile and repayment history.

This stage includes:

- Credit score check

- Income verification

- Employment or business verification

- Existing EMI assessment

- Bank statement review

A low credit score or high debt obligations may affect loan approval or the sanctioned amount.

Step 5: Property Legal and Technical Checks

The lender conducts legal and technical verification before approving the loan.

Legal Verification

The bank’s legal team checks:

- Property ownership

- Title clarity

- Encumbrance status

- Builder approvals

- Approved plans and permissions

Technical Verification

A technical valuer inspects:

- Construction quality

- Property condition

- Market value

- Carpet or built-up area measurements

- Construction stage

If issues are found during verification, the lender may reduce the loan amount or keep the application on hold.

Step 6: Receive the Home Loan Sanction Letter

Once verification is complete, the lender issues a home loan sanction letter. It mentions:

- Loan amount

- Interest rate

- Loan tenure

- EMI amount

- Terms and conditions

- Validity period

The sanction letter is a conditional approval and not the final disbursement.

Step 7: Sign the Loan Agreement

After accepting the sanction terms, the borrower signs the loan agreement and repayment mandate.

This stage may include:

- ECS/NACH setup

- Mortgage creation

- Submission of original property documents

- Disbursement request formalities

For under-construction properties, lenders may also require a tripartite agreement between the buyer, builder, and lender.

Step 8: Complete the Home Loan Disbursement Process

The final stage is loan disbursement. The lender releases the sanctioned amount directly to the seller or builder upon completion of all checks and mortgage formalities.

Disbursement can happen in two ways:

| Property Type | Disbursement Type |

| Ready-to-move property | Full disbursement |

| Under-construction property | Partial disbursement in stages |

What Is the Home Loan Processing Time in India?

The home loan processing time in India usually ranges from 7 to 15 working days for sanction and may take up to 30 days for final disbursement, depending on the lender, property type, and document verification process.

Here is a typical home loan timeline:

| Stage | Estimated Timeline |

| Application & Documentation | 1–3 days |

| Credit & KYC Verification | 3–5 working days |

| Legal & Technical Checks | 3–7 working days |

| Sanction & Disbursement | 1–3 weeks |

Several factors can affect home loan processing time, including:

- Documentation: Incomplete paperwork can delay approval.

- Applicant Profile: Self-employed applicants may take longer due to additional income verification.

- Property Type: Resale and under-construction properties often require more legal checks.

- Credit Score: Low credit scores may lead to additional scrutiny.

Application Mode: Digital applications are usually processed faster than offline applications.

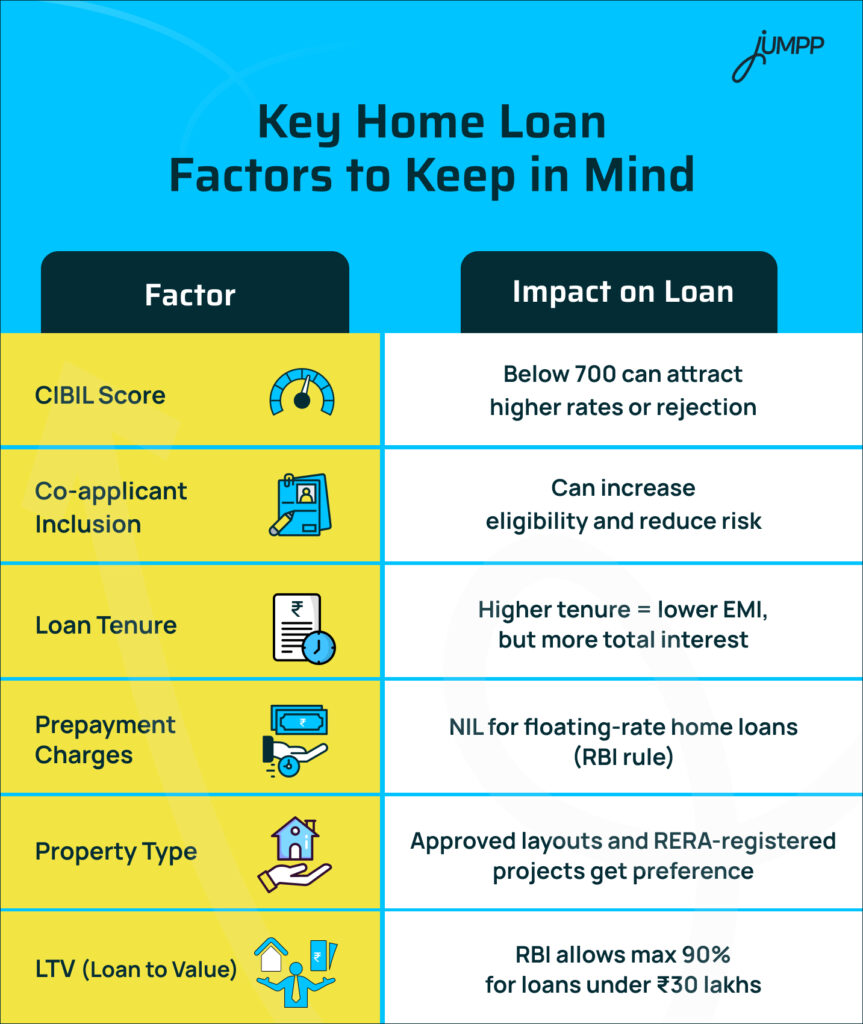

What Factors Affect Home Loan Approval?

Lenders consider multiple financial and property-related factors before approving a home loan, including eligibility, loan amount, interest rate, and repayment terms.

Here are some important home loan factors lenders evaluate:

Lenders also assess the Loan-to-Value (LTV) ratio, which determines how much of the property value can be financed through a home loan.

What Is the Home Loan Balance Transfer Process?

A home loan balance transfer allows borrowers to shift their existing home loan from one lender to another, usually to get a lower interest rate or better loan terms.

The home loan balance transfer process typically includes:

- Requesting a foreclosure letter from the current lender

- Applying for a balance transfer with the new lender

- Submitting income, KYC, and property documents

- Completing fresh credit and property verification

- Loan approval by the new lender

- Transfer of outstanding loan amount to the old lender

- Signing a new loan agreement

Home Loan Sanction vs Disbursement: What Is the Difference?

A sanction letter confirms that the lender is willing to provide the loan, subject to certain conditions. Disbursement happens only after all legal, technical, and documentation checks are completed.

| Basis | Home Loan Sanction | Home Loan Disbursement |

| Meaning | Loan approval from the lender | Release of the loan amount |

| Stage | After eligibility and verification | After agreement and mortgage formalities |

| Money Transfer | No funds are released | Funds are transferred to the seller or builder |

| Depends On | Income, credit score, documents | Property checks and legal completion |

| Validity | Valid for a limited period | Final stage of the loan process |

Common Mistakes to Avoid in the Home Loan Process

Home loan mistakes one must avoid are not checking your credit score, overstretching your budget, failing to compare lenders, and ignoring hidden fees.

Here are key mistakes to avoid:

- Applying without checking eligibility

Applying for a loan beyond your repayment capacity may result in rejection or a lower sanction amount. - Ignoring your credit score

A low credit score can affect approval chances and may result in higher interest rates. - Submitting incomplete documents

Missing income proofs, bank statements, or property papers can slow down verification and disbursement. - Not verifying property documents properly

Legal issues, missing approvals, or unclear property titles can delay or stop loan approval. - Taking on new debt before approval

New EMIs or credit card debt may affect your repayment capacity and eligibility. - Choosing a longer tenure only to reduce EMI

Lower EMIs may look comfortable initially, but a longer tenure increases the total interest paid over time. - Ignoring additional costs

Processing fees, legal charges, registration costs, insurance, and stamp duty should also be considered while planning the loan. - Not comparing lenders

Interest rates, processing timelines, and loan terms vary across lenders, so comparing options is important before applying.

Conclusion

Before applying, compare lenders carefully, evaluate your repayment capacity, and review the terms in detail. Knowing each stage of the home loan journey can help you avoid delays and make more informed financial decisions.

Once you are clear about your borrowing needs, explore the best loan app options on jUMPP to find what fits your repayment comfort.

Home Loan Process: FAQs

The home loan process includes application, document verification, credit check, loan sanction, property valuation, agreement signing, and disbursal as per bank policy.

To apply for a home loan, you need to submit identity proof, income documents, bank statements, and property papers. The lender verifies these before deciding on loan eligibility.

A 20 lakh home loan EMI typically ranges from approximately ₹16,000 to ₹18,000 per month for a 20-year tenure at interest rates of 8.5%–9.5% p.a.

With a ₹60,000 monthly income, you may be eligible for a ₹43–50 lakh home loan, based on your repayment capacity, liabilities, and credit score.

No, banks in India do not offer 100% home financing. As per RBI rules, you must pay a margin of 10% to 25% from your own funds.

With a ₹1 lakh salary, loan eligibility could range from ₹40–60 lakh. However, this is subject to tenure, credit history, and existing debts.