What is a Cancelled Cheque? How to Make, Write, Use and Submit

At some point, almost everyone is asked to submit a cancelled cheque, whether it is for a loan, salary account, or investment. And the first reaction is usually confusion. What exactly is a cancelled cheque? Why is it required? And how can something “cancelled” still be useful?

Understanding this simple document can save you from delays, rejections, and unnecessary back and forth with banks or employers.

What is a Cancelled Cheque?

A cancelled cheque is a regular cheque marked with two diagonal parallel lines and the word “CANCELLED” written across it, rendering it invalid for withdrawal but validating account details like name, account number, and IFSC code.

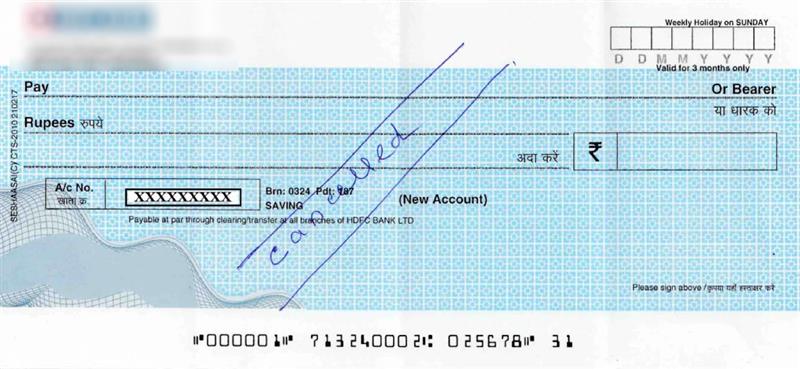

Cancel Cheque Sample

What is the Use of a Cancelled Cheque

A cancelled cheque is used as a supporting document in financial processes where verified bank details are required without enabling any debit transaction. It acts as a standard proof of banking information across multiple regulated activities.

- Investment onboarding: Required for starting mutual funds, SIPs, and opening Demat or trading accounts

- Loan processing: Used by lenders to link and validate the repayment account before approving credit

- Insurance and financial products: Submitted while purchasing policies to register the correct bank account

- Employee and payroll systems: Helps organisations map bank details accurately for salary and reimbursements

Managing payroll and employee benefits? Understand what is ESIC number and how it plays a crucial role in employee financial and insurance processes.

- EPF and retirement claims: Used during provident fund withdrawals to ensure funds are credited to the correct account

- Government and tax processes: Sometimes required for verifying bank details for refunds or benefit transfers

- Banking services setup: Helps in linking accounts for services like auto-debit instructions and standing mandates

A cancelled cheque is essentially a standard verification tool across financial ecosystems, ensuring processes are completed smoothly without errors in bank account details.

Open a zero-balance savings account online now!

Why is a Cancelled Cheque Required

A cancelled cheque is required to securely verify bank account details such as account number and IFSC, without allowing any transaction. It acts as proof that the account belongs to the individual and is active.

- Accuracy of bank details: Provides exact account number, IFSC, and MICR as printed by the bank, reducing manual errors

- Verification of ownership: Confirms that the bank account belongs to the person submitting it

- KYC compliance: Required during investments, insurance, and financial onboarding to prevent fraud

- Transaction safety: Marking it “CANCELLED” ensures it cannot be used to withdraw money

- Setting up auto payments: Used for EMIs, SIPs, ECS, and NACH mandates to enable automatic deductions

- Receiving payments: Helps employers, EPFO, and institutions credit salary, PF, or refunds correctly

- Financial processes: Commonly required for Demat accounts, mutual funds, loans, and tax-related transactions

Managing bank requirements goes beyond cheques and documentation.

Check how average monthly balance rules impact your account and avoid penalties

Common uses of a Cancelled Cheque

It is primarily used for KYC verification, KYC documentation, setting up Electronic Clearing Service (ECS) mandates, and salary or payout processing without risking funds.

How to Make a Cancelled Cheque

A cancelled cheque is created by marking a cheque leaf to share bank details like account number and IFSC safely, without allowing any transaction.

How to cancel a cheque- follow these steps-

- Pick a fresh cheque leaf: Take an unused cheque from your chequebook

- Draw lines: Draw two parallel diagonal lines across the cheque

- Label it: Write “CANCELLED” in capital letters between the lines

- Keep it clean: Ensure account number, IFSC, and MICR remain clearly visible

Is a signature required on a cancelled cheque?

No, a signature is not required and should not be added.

How to Write a Cancelled Cheque

Writing a cancelled cheque correctly ensures it is valid for verification and not misused for payments.

- Use proper ink: Write using a blue or black ballpoint pen

- No signature: Do not sign the cheque as it is not meant for transactions

- No other details: Do not fill payee name or amount fields

- Only one word: Write only “CANCELLED” in clear capital letters

How to Give a Cancelled Cheque

A cancelled cheque can be submitted either physically or digitally, depending on the requirement.

- Physical copy: Hand over the original cheque when submitting in person

- Digital copy: Upload a clear scanned image or photo in PDF or JPEG format for online processes

- Ensure clarity: The cheque image must be fully visible and readable

- Follow security: Share only with verified entities like banks, employers, or registered financial institutions

Adjustment and Management of Cancelled, Lost, or Lapsed Cheques

Handling cheques correctly is essential to maintain accurate financial records and prevent misuse. Whether a cheque is cancelled, lost, or expired, each situation requires a specific process along with proper accounting treatment.

Most financial processes today rely on proper KYC and verified details.

Check your Aadhaar update status to ensure your banking documents stay valid

Cancelled Cheques (Intentionally Voided)

A cancelled cheque is marked unusable, but still plays an important role in verification and documentation.

- Process: Draw two diagonal lines and write “CANCELLED” clearly across the cheque

- Record management: Keep a copy for audit trail and documentation purposes

- Disposal: Destroy unused originals carefully to avoid misuse

- Accounting treatment: Reverse or adjust the related entry if it was linked to a transaction

- Reissue handling: Issue a fresh cheque if required without duplicating charges

Lost or Stolen Cheques

Lost or stolen cheques carry a higher risk and require immediate preventive action.

- Immediate action: Inform the bank and request a stop payment without delay

- Formal reporting: File a complaint with the bank and lodge an FIR if required

- Proof: Obtain confirmation from the bank that the cheque has not been encashed

- Accounting treatment: Treat the cheque as cancelled in your books with proper documentation

- Reissue: Issue a new cheque only after obtaining indemnity from the payee

Lapsed or Stale Cheques

A cheque becomes lapsed when it is not presented within its validity period (generally 3 months in India as per current banking norms).

- Collection: Retrieve the expired cheque from the payee

- Cancellation: Mark it as cancelled and do not reuse or alter it

- Reissue: Always issue a fresh cheque instead of modifying the old one

- Accounting treatment: Reverse the original transaction and credit the amount back

Proper handling of these scenarios ensures financial accuracy, prevents duplicate payments, and maintains compliance with banking and audit requirements.

Disclaimer– The rankings and figures in this article have been compiled from multiple verified reports, credible news sources, and public financial data available as of 2026.

All values are approximate and may vary with newer updates, revisions, or changes in official records.

Cancelled Cheque – FAQs

A cancelled cheque is a cheque leaf marked with two diagonal lines and the word “CANCELLED” across it, making it invalid for transactions. It is used as proof of bank account details, like account number and IFSC.

To cancel a cheque, draw two diagonal lines and write ‘CANCELLED’ across it.

Take a fresh cheque leaf, draw two diagonal lines, and write “CANCELLED” in capital letters using blue or black ink. Do not sign or fill in any other details on the cheque.

It can be submitted physically by handing over the cheque or digitally by uploading a clear scanned copy. Ensure all bank details are clearly visible before submission.

Yes, it is safe because it cannot be used for withdrawals once marked cancelled. However, it should only be shared with trusted institutions since it contains sensitive account information.

It is called cancelled because marking it void makes it unusable for any financial transaction. The term also comes from banking practice, where processed cheques are marked cancelled.

It is used for KYC verification, setting up EMIs, SIPs, salary credits, and linking bank accounts for financial services. It ensures accurate bank detail verification.

A physical cancelled cheque is generally used once for a specific submission. A scanned copy may be reused across platforms if accepted by institutions.

A cheque is cancelled to safely share bank details or when a mistake is made on a cheque. Banks may also cancel cheques due to stop payment, fraud concerns, or account closure.

It should be shredded or cut into small pieces before disposal to protect sensitive information. Avoid discarding it in a readable form.

Yes, an FIR may be filed under cheating laws if fraud is involved, but most cheque bounce cases are handled under the Negotiable Instruments Act in court.

Each physical cheque is meant for one-time submission. A digital copy can be reused multiple times if accepted for verification purposes.