What Is a ULIP Plan? Full Form, Lock-in Period, Tax Rules & Benefits

Many people buy a ULIP plan assuming it guarantees high returns or works exactly like a mutual fund. But a ULIP is not just an investment product. It also includes life insurance, lock-in rules, market-linked risks, and charges that can affect your long-term returns.

So, how does a ULIP actually work?

In this guide, we explain how ULIPs work, their tax rules, lock-in period, and how they compare with other investment options.

What Is a ULIP Plan?

ULIP’s full form is Unit Linked Insurance Plan.

A Unit Linked Insurance Plan (ULIP) is a financial product that combines life insurance coverage with market-linked investment. Part of your premium provides insurance protection, while the remaining amount is invested in equity, debt, or balanced funds based on your chosen investment strategy.

For example, if you invest ₹1 lakh annually in a ULIP:

- One portion pays for life insurance coverage

- The balance is invested in equity, debt, or hybrid funds

What are the Key Features of ULIPs?

It offers flexibility in fund switching, returns on investment, and long-term financial planning.

Here are the detailed features:

- Market-Linked Returns

Returns depend on the performance of the selected equity, debt, or hybrid funds. - 5-Year Lock-in Period

ULIPs come with a mandatory five-year lock-in period before partial withdrawals are allowed. - Fund Switching Flexibility

Investors can usually switch between funds based on market conditions and risk appetite. - Long-Term Financial Planning

ULIPs are often used for goals like retirement, wealth creation, and future family expenses. - Transparency in Charges

Insurance companies disclose fund allocation, policy charges, and investment details clearly.

How Does a ULIP Plan Work?

Here is a simple step-by-step breakdown of how a ULIP works:

| Step | Process |

| 1 | Choose life cover and fund type |

| 2 | Pay the ULIP premium |

| 3 | Applicable charges are deducted |

| 4 | The remaining amount is invested in selected funds |

| 5 | Returns depend on market performance |

| 6 | Maturity or death benefit is paid |

Step 1: Choose Life Cover and Fund Type

The investor selects the life insurance cover and chooses where to allocate the investment, such as equity, debt, or balanced funds.

Step 2: Pay the ULIP Premium

Premiums can usually be paid monthly, quarterly, or annually based on the policy terms.

Step 3: Applicable Charges Are Deducted

Insurance companies deduct charges such as:

- mortality charges

- fund management charges (FMC)

- premium allocation charges

- policy administration charges

Step 4: Investment

After deductions, the remaining premium is invested in the selected market-linked funds.

Step 5: Returns Depend on Market Performance

The value of the investment fluctuates with market conditions and fund performance.

Step 6: Maturity or Death Benefit Is Paid

- On policy maturity, the fund value is paid to the policyholder.

- In case of the policyholder’s death during the policy term, the nominee receives the applicable premium according to policy terms.

What Is the Lock-in Period in ULIP?

ULIPs come with a mandatory 5-year lock-in period, which means investors cannot fully withdraw their funds before the 5-year mark from the policy start date.

During the lock-in period:

- Partial withdrawals are restricted

- Surrendering the policy may attract discontinuation charges

- The investment remains locked until the completion of five years

After the lock-in period ends, policyholders may be permitted to make partial withdrawals under the insurer’s terms and conditions.

What Are the Types of ULIP?

ULIPs can be categorised based on investment preference, premium payment structure, and financial goals.

1. Types of ULIPs Based on Investment

| ULIP Type | Risk Level | Suitable For |

| Equity ULIP | High | Long-term wealth creation |

| Debt ULIP | Lower | Conservative investors |

| Balanced ULIP | Moderate | Balanced risk and return approach |

- Equity ULIP: Invests mainly in equity markets and may offer higher long-term return potential with higher market risk.

- Debt ULIP: Invests in fixed-income instruments like bonds and government securities with relatively lower risk.

- Balanced ULIP: Invests in both equity and debt instruments to balance growth and stability.

2. Types of ULIPs Based on Premium Payment

| Premium Type | Meaning |

| Single Premium ULIP | One-time lump sum investment |

| Regular Premium ULIP | Premium paid periodically |

- Single Premium ULIP: The investor pays a single premium at the beginning of the policy term.

- Regular Premium ULIP: Premiums are paid monthly, quarterly, or annually throughout the policy period.

3. Types of ULIPs Based on Financial Goals

| Goal-Based ULIP | Purpose |

| Child ULIP Plan | Future education or child-related goals |

| Retirement ULIP Plan | Retirement planning and long-term savings |

| Wealth ULIP Plan | Long-term wealth creation |

4. Other Ways ULIPs Are Categorised

Some ULIPs promise a minimum return or capital protection, while others are fully market-linked with no guaranteed amount. Guaranteed ULIPs usually come with higher charges.

This classification refers to how an insurance payout is made upon death.

- Type 1 pays either the sum assured or the fund value, whichever is higher.

- Type 2 pays both the sum assured and the fund value, making it more suitable for people seeking greater financial security for their family.

Want to understand how ULIPs compare with traditional policies? Learn more in our guide on what is life insurance.

What Are the Tax Benefits of ULIP?

ULIPs offer tax benefits under different sections of the Income Tax Act, subject to applicable conditions.

| Tax Benefit | Applicable Section |

| Tax deduction on the premium paid | Section 80C |

| Tax-free maturity proceeds | Section 10(10D) |

| Tax-free fund switching | No immediate capital gains tax |

Here are some important ULIP tax rules investors should know:

- Premiums paid toward ULIPs may qualify for deductions under Section 80C, subject to the prescribed limit.

- Maturity proceeds may remain tax-free under Section 10(10D), subject to eligibility conditions.

- Fund switching within a ULIP is generally not taxed immediately.

- For ULIPs issued on or after February 1, 2021, maturity proceeds may become taxable if the annual premium exceeds ₹2.5 lakh.

Along with tax planning, also check the cash deposit limits of your savings account!

What Are the Advantages and Disadvantages of ULIP?

Key advantages of ULIP include flexibility to switch between equity/debt funds, and a lock-in to promote long-term discipline. However, they come with disadvantages like high upfront fees, market volatility risks, and limited liquidity during the initial years.

| ULIP Advantages | ULIP Disadvantages |

| Combines insurance and investment in one plan | Mandatory 5-year lock-in period |

| Market-linked growth potential | Returns are not guaranteed |

| Fund switching flexibility | Can be complex for beginners |

| Suitable for long-term financial goals | Limited liquidity during lock-in |

| Transparent NAV and fund tracking | Not ideal for short-term investing |

What are Mortality Charges in ULIP?

Mortality charges in a ULIP are the fees deducted by the insurance company to provide life insurance coverage under the plan. These charges are deducted regularly from the premium or fund value during the policy term.

The mortality charge usually depends on factors such as:

- age of the policyholder

- sum assured

- policy tenure

- health and lifestyle profile

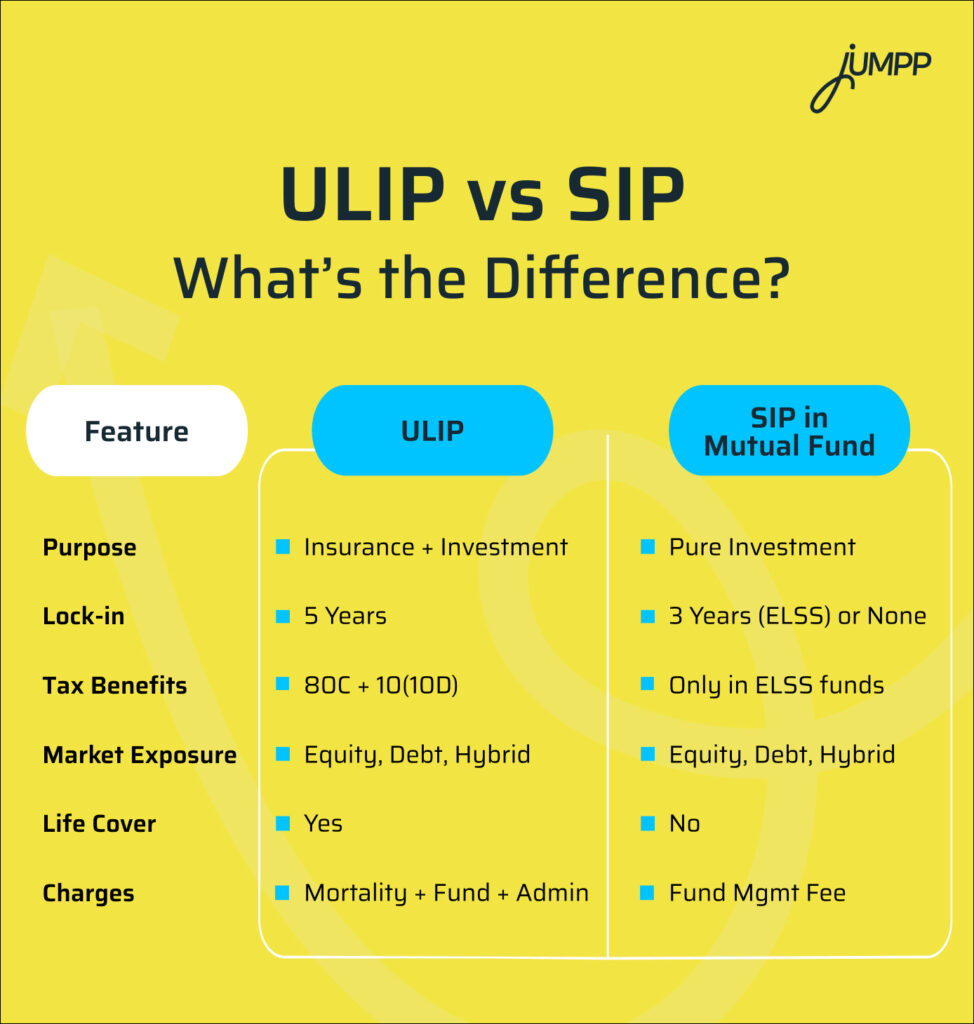

ULIP vs SIP: What’s the Difference?

This is a question many Indian investors ask: ULIP vs SIP – which is better?

SIP is great for those who want pure investment returns, flexibility, and liquidity.

ULIP is better suited for investors who want market participation with a protection layer and are ready for a long-term commitment.

Start investing in SIPs, mutual funds, FDs, and Digital Gold—get started with our Investment App

What Is the Difference Between a ULIP and a Mutual Fund?

ULIPs may suit investors looking for both insurance protection and long-term investing in one plan. Mutual funds are generally preferred by investors seeking market-linked investments without an insurance component.

| Feature | ULIP | Mutual Fund |

| Insurance Cover | Includes life insurance | No insurance coverage |

| Investment Type | Insurance + investment product | Pure investment product |

| Lock-in Period | Mandatory 5-year lock-in | Depends on fund type |

| Returns | Market-linked | Market-linked |

| Tax Benefits | Available under Sections 80C and 10(10D) | Depends on the fund category |

| Fund Switching | Usually allowed within the plan | Redemption and reinvestment required |

| Charges | Includes insurance and policy charges | Primarily fund management charges |

| Suitable For | Long-term goals with insurance needs | Wealth creation and investment-focused goals |

Common Myths About ULIPs

Myth 1: ULIPs are very expensive.

While older ULIPs had high charges, modern plans are much more cost-efficient, especially digital ULIPs.

Myth 2: ULIPs don’t give good returns.

Returns depend on fund performance and holding period. With a 10+ year horizon, many ULIPs have matched mutual fund performance.

Myth 3: ULIPs are complicated.

With digital dashboards, transparent fund switching, and real-time tracking, managing a ULIP is now as easy as handling a mutual fund SIP.

Conclusion: Should You Invest in ULIP?

If you’re looking for a disciplined, long-term investment that combines life cover and market participation, a ULIP can be a powerful tool in your portfolio. But you must stay invested for at least 10-15 years to truly benefit from compounding and fund growth. And you must be clear: ULIPs are not short-term products or alternatives to pure term plans.

As you plan investments and premium payments online, know the difference between UPI and net banking to manage your digital transactions easily.

ULIPs- FAQs

ULIPs can be classified by investment type, payment mode, and goal. Some of the most common types include equity, debt, balanced, child, and retirement ULIPs.

In a Type 2 ULIP, your nominee gets both the sum assured and the fund value in case of death. This offers higher financial protection than Type 1.

The main charges are premium allocation, policy administration, fund management, mortality, and surrender or withdrawal charges. These vary by insurer and plan.

Most ULIPs offer 5 to 8 fund options, including equity, debt, and balanced choices. You can switch between them based on your risk and goals.

ULIP stands for Unit Linked Insurance Plan. It combines life insurance with investment in market-linked funds like equity or debt.

Yes, if you want long-term growth with life cover and tax benefits. It works best when you stay invested for 10 years or more.

ULIP has a 5-year lock-in, but 5 years is the bare minimum. You should ideally invest for 10 to 15 years to see strong returns.

ULIPs have a mandatory lock-in period of 5 years. During this period, full withdrawals are not allowed, and partial withdrawals are restricted based on policy terms.

ULIP returns depend on the performance of the selected equity, debt, or balanced funds. Since ULIPs are market-linked products, returns are not guaranteed.

FMC stands for Fund Management Charges. These are fees charged by the insurer for managing the investment funds within a ULIP plan.