Coinsurance Meaning: The Clause That Affects Your Hospital Bill

When most people in India think about health insurance, they believe that the insurer will cover the full and final hospital bill. But in practice, one of the lesser-known but crucial aspects of a health insurance policy is coinsurance. If you are wondering about coinsurance’s meaning, it refers to the percentage of the medical bill that you, the policyholder, are required to pay after the deductible is met.

In this blog, we will introduce you to the overall concept of coinsurance in India.

What is Coinsurance in Health Insurance

Coinsurance means cost-sharing between you and the insurance company. After you have paid your deductible (the fixed amount you pay first), you and your insurer split the remaining costs in a fixed percentage.

Hospitals calculate how much of the bill goes to the insurer and what portion you must pay.

The percentage (10%, 20%, etc.) is defined in your policy at the time of purchase.

Example

Suppose your health insurance includes:

- Coinsurance → 20%

- Deductible → ₹10,000

- Hospital bill → ₹1,00,000

Calculation:

Pay deductible → ₹10,000

Remaining bill → ₹90,000

Coinsurance (20% of ₹90,000) → ₹18,000

Total paid by you → ₹28,000

Insurance company pays → ₹72,000

What is a Deductible in Health Insurance?

A deductible is the fixed amount you must pay out of pocket before your health insurance starts covering the remaining hospital expenses.

For example, if your deductible is ₹10,000 and your hospital bill is ₹80,000, you first pay ₹10,000. The insurer then covers the remaining ₹70,000, as per policy terms.

Many top-up and super top-up health plans in India include deductibles to lower premium costs.

Key Points:

- Deductible is the first expense.

- You pay it before the insurer covers the rest.

- The higher the deductible, the lower your premium, but the more you pay during hospitalisation.

If you’re healthy and want to reduce your premium, a higher deductible policy might make sense. But if you want full financial protection, you can choose a policy with a low or zero deductible.

Check the different types of health insurance in India before you make your decision.

What is Copayment in Health Insurance?

A copayment (copay) is a fixed amount you pay each time you use a medical service, regardless of the total bill amount.

For example, if your policy has a ₹1,000 copay per hospitalisation, you pay ₹1,000 whether the bill is ₹25,000 or ₹2,50,000. The insurer covers the remaining eligible amount as per policy terms.

Key Points

- Fixed amount per claim or service

- Paid every time you use medical services

- Separate from deductible and coinsurance

- Applies regardless of total bill size

Common Cases Where Copay Applies

- Senior citizen health policies

- OPD treatment coverage

- Treatment at non-network hospitals

- Some group insurance plans

Why Do Insurance Companies Use Coinsurance?

Coinsurance helps insurers manage risk in several ways:

- If policyholders know they must pay a part of the bill, they are more likely to avoid unnecessary or overpriced treatments.

- By adding coinsurance, insurers can offer lower premiums while still protecting against major medical events.

- Especially for senior citizens or in high-risk categories, coinsurance helps balance the cost between the policyholder and the insurer.

How Coinsurance Works in India

Coinsurance in India may vary depending on the type of hospital you choose for treatment.

Network Hospitals

In India, most health insurance companies have a list of hospitals where you can get cashless treatment. These are called network hospitals.

- Usually lower coinsurance rates (e.g., 10%)

- Cashless treatment available

- You only pay your share (deductible, copay, coinsurance)

The insurer directly settles the remaining bill with the hospital.

Non-Network Hospitals

But if you go to a non-network hospital, you may have to pay the entire bill upfront and later file for reimbursement.

- Higher coinsurance rates may apply (e.g., 20%)

- The full bill is often paid upfront by you

- Reimbursement claim required later

Because reimbursement is involved, your out-of-pocket amount may feel higher during the claim process.

Always check hospital network terms before admission, as coinsurance clauses can differ between network and non-network facilities.

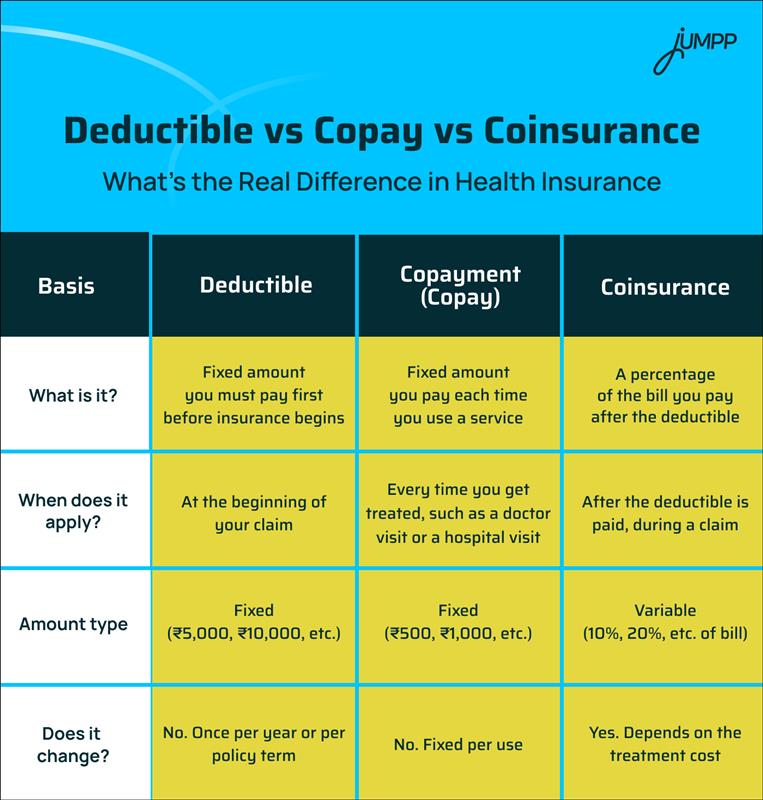

Deductible vs Copay vs Coinsurance: Key Differences

These three terms define how much you pay out of pocket during a medical claim.

Here is how they differ:

Summary:

- Deductible → First amount you pay

- Copay → Fixed charge per visit

- Coinsurance → Percentage of remaining bill

Example

Hospital Bill → ₹1,00,000

Deductible → ₹10,000

Coinsurance → 20%

Copay → ₹1,000

You pay:

- ₹10,000 (deductible)

- ₹18,000 (20% of ₹90,000)

- ₹1,000 (copay)

Total paid by you → ₹29,000

Insurance pays → ₹71,000

What Happens After You Reach Your Coinsurance Limit?

Once your total payments for deductibles, copays, and coinsurance reach a set amount called the out-of-pocket maximum, you stop paying. From that point till the end of the policy year, your insurer covers 100% of all approved medical costs.

Whether it is another hospitalisation or follow-up treatment, you will not have to pay anything extra. This limit provides financial relief during serious or recurring health issues. It serves as a final safety net for your personal medical expenses.

Pros and Cons of Coinsurance

| Pros | Cons |

| Helps reduce premium cost | Can lead to high out-of-pocket expenses during emergencies |

| Encourages responsible use of medical services | May confuse new policyholders due to technical terms |

| Often includes an out-of-pocket maximum cap | Coinsurance rates may differ for network vs non-network hospitals |

| Makes higher coverage plans more affordable | Requires maintaining an emergency fund for claims |

Should You Choose a Policy with Coinsurance?

It depends on your financial goals and risk comfort.

You may choose coinsurance if:

- You are young and healthy

- You rarely visit hospitals

- You want to save on premiums and don’t mind paying a share during a rare emergency

You should avoid coinsurance if:

- You have a family with senior members or chronic health issues

- You want full coverage, even if it means a higher premium

Final Checklist Before Buying Health Insurance

Before buying a policy, make sure you ask these questions:

- What is the coinsurance percentage, and when does it apply?

- Is there a deductible? If yes, how much?

- Does the policy include a copayment?

- What is the out-of-pocket maximum?

- Are the rates different for network vs non-network hospitals?

- Does the coinsurance apply per claim or per policy year?

- Does the policy cover OPD or just hospitalisation?

Final Thoughts

Coinsurance directly affects how much you pay during a medical emergency. And in a country like India, where healthcare costs are rising, knowing how your policy works is crucial.

When choosing health insurance, do not just look at the coverage amount or the premium. Ask yourself:

- What happens during a claim?

- How much do I really pay out of my own pocket?

Remember, insurance is not just about affordability. It is about assurance.

Coinsurance Meaning: FAQs

Coinsurance means you share a part of the medical bill with your insurer after the deductible is paid. It’s usually shown as a percentage like 10% or 20%.

It means your insurer will pay 80% of the eligible claim amount. You will pay the remaining 20% out of pocket.

Coinsurance is a percentage of the bill you pay, while a copay is a fixed amount per service. Both are cost-sharing clauses, butthey work differently.

A deductible is a fixed amount you must pay first before the insurer pays anything. Coinsurance applies after that, based on the remaining bill.

This is the maximum amount you may need to pay as coinsurance in a policy year. After this, the insurer pays 100% of the remaining covered costs.

If your policy has a ₹1,000 copay per hospital visit, you always pay ₹1,000, whether the total bill is ₹10,000 or ₹1,00,000.

Coinsurance, copay, and deductible are all cost-sharing terms in health insurance. A deductible is what you pay first. A copay is a fixed fee per service. Coinsurance is the percentage you split with the insurer after the deductible is paid.