Differences Between NEFT, RTGS and IMPS: Meaning, Charges, and Limits

We have all faced situations where UPI does not work, either because the daily limit has been or the amount is too large to transfer. At that moment, the other familiar bank transfer methods such as NEFT, RTGS and IMPS come to mind. But do you really know the difference between NEFT, RTGS and IMPS, and when each one should be used?

Here is the simplest way to remember:

- NEFT is ideal for scheduled or routine transfers.

- RTGS is best for high-value, real-time payments.

- IMPS is the instant 24×7 option for urgent money movement.

Understanding how these three modes differ in speed, limits and charges helps you choose the right method for your transaction.

Let us break it down clearly.

IMPS vs NEFT vs RTGS: Know Your Options Before Your Next Big Transfer

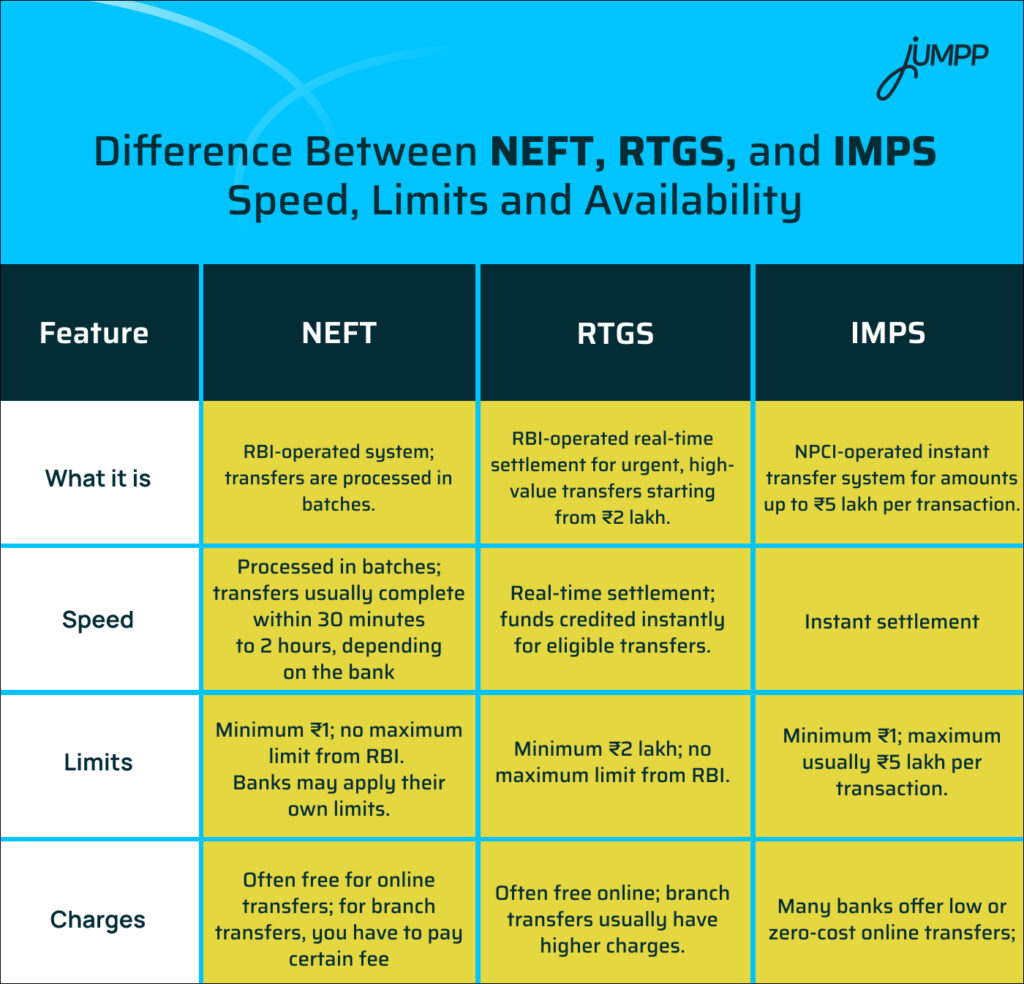

All three services, NEFT, RTGS and IMPS, are available 24×7×365, including Sundays and bank holidays, for online transactions.

Here is the basic difference between NEFT vs. RTGS vs. IMPS:

Note: Limits and charges may differ across banks and digital channels in 2026.

What is NEFT in Banking?

The full form of NEFT in banking is National Electronic Funds Transfer. It is an RBI-regulated system for secure bank-to-bank transfers in India.

How NEFT Works

The NEFT payment system works in the following manner-

- Initiation: You need to enter the beneficiary’s account number, IFSC code, and amount in your bank’s net banking or mobile app.

- Batch Processing: Banks send transaction details to the RBI, which processes them in half-hourly batches.

- Settlement: Funds are settled through deferred net settlement, then credited to the beneficiary’s account.

How to Transfer Money via NEFT

Here are the quick steps that you must follow-

- Log in to net banking or mobile banking.

- Enter beneficiary details and amount.

- Confirm and authorise with OTP.

NEFT Timings (2026 Update)

| Method | Timing | Notes |

| Online Transfers | 24×7×365 | NEFT remains available round-the-clock in 2026, including Sundays, bank holidays, and national holidays. |

| Batch Processing | Every 30 minutes | Transactions are settled in half-hourly batches throughout the day, including after banking hours. |

NEFT Limits & Charges

| Basis | Details |

| Minimum amount | ₹1 per transaction |

| Maximum amount | No upper limit as per RBI, but banks may set their own cap |

| Charges | Often free online; branch transfers may attract small fees |

What are the Benefits of NEFT

Here is why you should opt for NEFT transfers-

- 24×7 availability for online transfers.

- Nationwide coverage connecting all participating banks.

- Secure and reliable platform for transactions.

- Versatile usage: salary, rent, EMIs, online purchases, etc.

- Accessible via net banking, mobile apps, and branches.

Who Regulates NEFT?

The Reserve Bank of India (RBI) owns and operates the NEFT system, ensuring secure and smooth interbank transfers.

What is RTGS in Banking?

The full form of RTGS in banking is Real-Time Gross Settlement.

“Real Time” means that transactions are processed immediately. “Gross Settlement” means that each fund transfer is settled individually.

- The funds are settled in the books of the Reserve Bank of India (RBI).

- This ensures the security and finality of transactions.

- RTGS is used for instant high-value transfers above ₹2 lakh.

How RTGS Works

RTGS payment mode works in the following manner-

- Provide Beneficiary Details: You need to enter the recipient’s account number, name, bank, branch, and IFSC code.

- Initiate Transaction: Specify the amount and authorise the transaction via your bank’s secure channel.

- Real-Time Processing: Funds are transferred immediately and settled individually in RBI books.

- Confirmation: Your bank confirms once the funds reach the beneficiary’s account, typically within a few minutes, though delays of up to 30 minutes may occur in rare cases.

What are the Different Ways to Initiate RTGS?

- Online Banking: Log in, select RTGS, enter beneficiary details, and submit.

- Mobile Banking App: You can use your bank’s app to make RTGS transfers quickly.

- Bank Branch: Fill out a form at the branch, and the staff will process the transfer for you.

RTGS Transaction Limits & Charges (2026 Update)

| Basis | Details (2026) |

| Minimum Transaction Amount | ₹2,00,000 |

| Maximum Transaction Amount | No upper limit set by RBI; banks may apply their own caps |

| Outward Charges | For branch-based transactions, banks may charge up to: • ₹2–5 lakh: up to ₹25 (excluding tax) • Above ₹5 lakh: up to ₹50 (excluding tax). Online RTGS is often free, depending on the bank |

| Inward Transactions | Free for all customers |

| Time to Credit | Real-time settlement, typically within 30 minutes |

| Failed Transactions | Amount is returned within 1 hour or by the end of the RTGS business day |

What is IMPS in Banking?

IMPS ( Immediate Payment Service) is a fast and secure way to transfer money 24/7 across banks via NPCI. It is ideal for small-value, instant transfers up to ₹5 lakh.

How IMPS Works?

IMPS method of payment works in the following manner-

- Register & Link Accounts: Both the sender and the receiver register with their banks and link their mobile numbers to their accounts.

- Initiate Transfer: Use mobile banking or internet banking; select IMPS, enter recipient details (mobile/MMID or account/IFSC) and amount.

- Authorise Transaction: Enter MPIN or net banking password to confirm.

- Receive Confirmation: Sender and receiver get instant notifications once funds are credited.

IMPS Charges & Limits (2026 Update)

| Transaction Amount | Charges (Excluding GST) |

| Up to ₹10,000 | ₹2.5 |

| ₹10,001 – ₹1,00,000 | ₹5 |

| ₹1,00,001 – ₹2,00,000 | ₹15 |

| Daily Limit | ₹5,00,000 as per NPCI guidelines; banks may set lower caps |

Availability: 24×7, all days of the year.

Transfer Speed: Funds are credited instantly upon approval.

Resolution Time: In rare cases of failures, resolution may take up to 5 working days.

What are the Benefits of IMPS

- You can do instant fund transfers anytime, anywhere.

- It offers secure transactions using MPIN, mobile number, or card PIN.

- IMPS has a wide coverage. It is supported by over 900 banks and PPI providers.

- It supports multiple channels, mobile apps, internet banking, and ATMs.

- It is ideal for online shopping, bills, and sending money to friends/family.

What Is the Impact of GST on NEFT, RTGS and IMPS Fees?

GST applies only to the service fees charged by banks, not the money you transfer.

Here’s what that means in practice-

- What’s Taxed: Only the service or processing fee charged by the bank is taxed.

- What’s Not Taxed: The actual amount you transfer is not subject to GST.

- No Fees, No GST: If your bank does not levy a transaction fee (for example, free IMPS transfers), then no GST is charged.

| Service | Post-GST Tax Rate | Impact |

| RTGS (Real-Time Gross Settlement) | 18% (GST) | Marginal increase in transaction costs due to the higher tax rate. |

| IMPS (Immediate Payment Service) | 18% (GST) | IMPS (Immediate Payment Service): GST is applicable only on the service fee charged by banks, resulting in a marginal increase in transaction cost where fees are levied |

| NEFT (National Electronic Funds Transfer) | 18% (GST) | Modest increase in NEFT transaction fees as a result of GST. |

If a bank charges ₹10 for an NEFT transaction, the customer will pay ₹10 + 18% GST = ₹11.80.

Advantages and Disadvantages of NEFT, IMPS, and RTGS

Like every payment method, NEFT, RTGS, and IMPS come with their own set of advantages and disadvantages that can affect which one you choose.

| System | Pros | Cons |

| National Electronic Funds Transfer (NEFT) | – Cost-effective. – No minimum limit – High security – 24/7 availability | – Not instant – Processing delays – Dependence on batch timing |

| Real-Time Gross Settlement (RTGS) | – Instant transfers – No upper limit – Highly secure – Immediate clearing | – High minimum limit – Higher charges – The transaction cannot be reversed. |

| Immediate Payment Service (IMPS) | – Instant transfers – 24/7 availability – Multiple access channels – Wide acceptance | – Maximum transaction limit – Transaction charges – Dependent on the bank’s – Daily limit |

Manage payments and track savings more efficiently with an AI-backed money management app.

What are the Safety Tips for Online Transfers?

Before sending money, a little caution goes a long way:

- Always check the beneficiary details, name, account number, and IFSC twice, maybe even thrice. One small mistake can be painful to fix.

- Stick to your own devices and trusted networks. Public Wi-Fi and random devices are a recipe for trouble.

- Turn on two-factor authentication. That extra step may feel like a hassle, but it can save you from the unexpected.

- Keep your banking info private. No one should ever have your PIN, password, or OTP.

- Use only official apps or websites. Avoid shortcuts through third-party platforms; you don’t want surprises.

Conclusion

NEFT, RTGS, and IMPS are the backbone of India’s electronic fund transfer system. NEFT is ideal for routine, RTGS is designed for high-value, and IMPS offers instant 24×7 transfers for small to medium amounts up to ₹5 lakh.

Now, you are all set to choose the right method for every situation.

Want smooth transfers with NEFT, RTGS, and IMPS? Open a zero balance saving account online and enjoy secure banking anytime.

Source– rbi.org.in

NEFT vs RTGS vs IMPS- FAQs

Choosing the “best” service depends on your needs: IMPS is instant for small to medium amounts (up to ₹5 lakh), RTGS is for instant high-value transactions (over ₹2 lakh), while NEFT is best for non-urgent transfers of any amount, processed in batches.

RTGS is immediate, while NEFT settles in batches, not instantly.

From 15 February 2026, online IMPS transfers above ₹25,000 will incur service charges when done via internet banking, mobile banking, or YONO, i.e. ₹25,000 – ₹1 lakh: ~₹2 + GST, ₹1 lakh – ₹2 lakh: ~₹6 + GST, and ₹2 lakh – ₹5 lakh: ~₹10 + GST.

NEFT through SBI net banking, mobile banking, or YONO is generally free for SBI savings account holders. If NEFT is done at a branch counter, SBI may levy charges depending on the amount transferred.

Google Pay is a Unified Payments Interface (UPI) app, which is an instant payment system built on top of IMPS, not NEFT or RTGS.

UPI is separate from NEFT and RTGS and operates as an instant payment system, primarily using IMPS for fund transfers.

NEFT (National Electronic Funds Transfer) is used to transfer funds electronically from one bank account to another across India.

NEFT processes transactions in half-hourly batches, making it suitable for smaller, non-urgent transfers. RTGS (Real-Time Gross Settlement) processes transactions in real time. It is ideal for high-value, urgent transfers.

The minimum amount for RTGS transactions is ₹2 lakh, with no upper limit set by the RBI.

NEFT is suitable for scheduled, non-urgent transfers and operates in batches, while IMPS (Immediate Payment Service) offers instant, 24×7 fund transfers, making it ideal for urgent, small-value transactions.

There is no maximum limit for NEFT transactions set by the RBI.